TVMIX exposes the Biden Family and The State Banks of the Chinese Communist Party.

JOE BIDEN said this of HUNTER’s business deals:

“I have never spoken to my son about his overseas business dealings.”

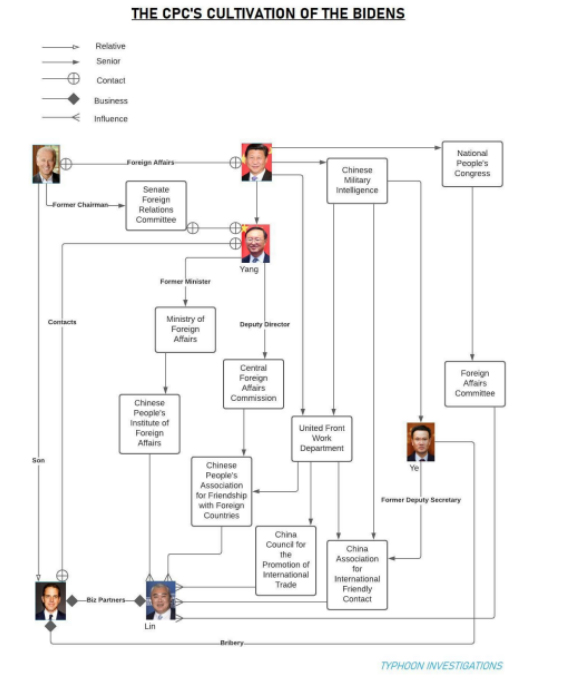

Our research shows clear intent by Chinese state officials acting to influence The Bidens either in official positions or with close relationships to them.

Joe Biden with son, Hunter Biden

Our research shows virtually all Biden financial investors or partners in China are state policy entities, state-owned entities, or only nominally private. The investments flow primarily to Chinese state backed projects or firms.

The financial terms, where we have been able to locate specific deal terms, engage in non-normal business practices designed to funnel fees and assets to benefit a specific party.

This facilitated use of Chinese state offices and officials to meet HUNTER and arrange for public money via the social security, local state-owned enterprises, and policy bank to fund the investment partnership.

Though the investment partnership was not official until late 2013, the key relationships and visits with companies and individuals who would become investors and partners began significantly earlier.

China invests large amounts of financial and political capital in influencing foreign individuals and institutions.

China invests large amounts of financial and political capital in influencing foreign individuals and institutions.

Given the personal connection with senior individuals within the Chinese government, there is absolutely no chance this investment partnership was undertaken as a normal market transaction or that political influence by Chinese was ignored.

Notably, key individuals have strong links to Chinese influence organizations.

Importantly, throughout the Obama administration BIDEN maintained a positive view of China. At an official dinner BIDEN said about Chairman Xi: Mr. President, the many hours we’ve spent together – we have had countless private discussions that go well beyond the typical talking points. And I came away – and I told the

President this after our multiple meetings, that I came away impressed with the president’s candor, determination, and his capacity… Both sides accept that we each gain more from

working together than our interest – and our interest – where our interests align than working alone, by addressing the differences candidly.

BIDEN has denied any knowledge of his son’s business activities in China or that it influenced any policy. Given the numerous official trips, Secret Service protection received by Hunter for unofficial trips, quasi-official receptions in Beijing, and press coverage it strains all credibility to accept these denials as reliable. At very least it is ethically problematic for the children of senior administration

personnel to be engaging in financial transactions with foreign governments, a transaction that would be disallowed for the parent. Even if a specific policy was not altered at the request of China, it clearly compromises the public official.

2010 Hunter Courts Chinese State Money – On April 12 and 13, BIDEN met with then Chinese President Hu Jintao (胡锦涛) in Washington as part of the Nuclear Security Summit。

Just a few days prior, between April 7 and 9, HUNTER took a business trip to Beijing where he joined Thornton’s LIN and BULGER for several meetings with some of China’s most powerful state financial institutions. The English news item is no longer accessible on Thornton’s website, but the Chinese

version remains.

According to Thornton’s news item, HUNTER was introduced as the chairman of Rosemont Seneca and the second son of the US Vice-President, and the purpose of his visit was to “deepen mutual understanding and explore the possibility of commercial cooperation”.

HUNTER visited multiple parties in one day, with each meeting appearing to last no more than one hour or two. It is unclear what meaningful discussions could have taken place during the short space of time, other than for Thornton to deliver HUNTER to their Chinese counterparties and flaunt their US political connections. Regardless of HUNTER’s intentions, his hosts treated his visit at a quasi-state level.

In chronological order, HUNTER met with the following Chinese financial institutions:

• National Council for Social Security Funds

• Hillhouse Capital

• China-United States Exchange Foundation

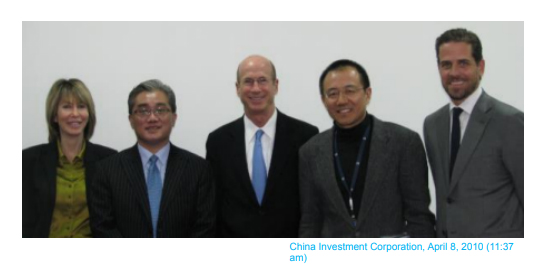

• China Investment Corporation

• China Life Insurance (Group) Company

• Postal Savings Bank of China

• Founder Group

2011 From April 18 to April 20, HUNTER visited leading Taiwan banks and financial institutions, along with Thornton Chairman BULGER and CEO LIN. 3 HUNTER was introduced this time as a senior consultant of Rosemont Realty. In 2010, Rosemont Realty acquired BGK, which owned 135 commercial buildings in 22 states. Burrell was appointed CEO, and HUNTER was appointed to the board of advisors. Rosemont Realty’s website is no longer accessible, but archived records show HUNTER was listed as an advisor in 2011. 4 FOIA records show that after departing Taiwan, HUNTER visited China, staying there until April 22. There are no media reports on the purpose of his visit.

2012 Hunter’s First China Deal – Wanxiang On February 17 2012, BIDEN met with Xi, then Vice-President (but soon to be China President) in California.

By BIDEN’s count, he met with Xi for a rough total of 25 hours in 2011 and 2012.

One topic of discussion was access for US film companies in the China market.

On February 19, HUNTER’s Seneca Global Advisors advised GreatPoint, a US energy technology start up in receiving an equity investment of USD 420 million and project funding of USD 1.25 billion from Wanxiang Group (万向集团) , the largest foreign venture capital investment into the US that year.

The two parties agreed to jointly-develop a coal-to-natural gas facility in Xinjiang (an autonomous territory in northwest China). The signing ceremony was attended by senior US and Chinese government officials, such as Xi.

It belies any credibility for BIDEN to claim no knowledge of his son’s business activities with China with these types of ceremonies. These types of political ceremonies also raise valid questions about policy influence from Hunter business activities. Wanxiang founder Lu Guanqiu (鲁冠球), had met with Obama in January 2011, and employed Obama’s ally, former Chicago Mayor Richard Daley.

HUNTER had previously worked for Richard’s brother Secretary of Commerce William Daley, as Executive Director of E-Commerce Policy Coordination.

HUNTER had previously worked for Richard’s brother Secretary of Commerce William Daley, as Executive Director of E-Commerce Policy Coordination.

William Daley was Obama’s former Chief of Staff (2011 – 2012). Wanxiang is a long-established and politically well-connected industrial conglomerate based in Hangzhou, where Lu knew Xi from Xi’s days as Zhejiang CPC Secretary in the early 2000s (and Xi’s father in the 1980s). Following the millions given to Massachusetts based GreatPoint, Wanxiang appears to have benefited from US policy decisions where BIDEN was involved: In 2013, Wanxiang acquired the bankrupt assets of A123 Systems Inc , and in 2014, won a bankruptcy auction for the assets of Fisker Automotive , the defunct manufacturer of the Karma plug-in hybrid sports car.

Both Fisker and A123 were funded in part with US government loans to build cars in Delaware, BIDEN’s home state, which meant Wanxiang obtained technology developed with US taxpayer money. An investigative report said BIDEN’s administration pushed for the loans in 2009.

Bankruptcy filings show HUNTER was also listed as a Fisker creditor, meaning he either had put down a deposit for a car, or was an early investor.

Wanxiang also picked up a GM plant from the Fisker purchase, and sensitive technology from the A123 acquisition, that could be put to use by the Chinese military.

Wanxiang is active in China’s foreign influence operations, including paying for Delaware students to study Mandarin in China.

Wanxiang supports the Chinese government’s investments in North Korea, where it owns a major copper mine.

Wanxiang’s imports also support the North Korean regime, and despite being one of the largest importers of North Korean minerals, it has so far managed to evade US sanctions which have ensnared its smaller competitors during Obama’s presidency.

2012 – 2013 Hunter’s Second China Deal – BHR

At some point during 2012, according to US and Chinese media reports, the catalyst for HUNTER’s first deal in China was when the Bohai Capital CEO Jonathan Li, Li Xiangsheng (李祥生) visited New York at an unspecified time in 2012 and met with ARCHER to discuss finding a suitable investment partner.

“Don’t you think that I’m the most suitable business partner for you?” Archer told Li as they smoked cigars in a Manhattan bar, according to an account in the 21st Century Business Herald, a Communist Party-owned newspaper.

“Companies globally all like to have powerful people on the board as these connections help raise capital, smooth joint ventures, and add outside insight,” said Andrew Collier, managing director of Orient Capital Research, a Hong Kong-based consulting firm. Archer was “very convincing,” the story said, in part because Archer’s

company “has a deep network of contacts in U.S. political circles. R. Hunter Biden, the son of U.S. Vice President Biden, is one of the company’s executives.” “China is particularly connection-heavy because government relations often spell the difference between success and failure, both in raising money and in getting

contracts,” he said. “It’s not clear that Hunter Biden did anything more than put his name on the door of this particular company.”

Washington Post, October 13, 2019

Our research shows that HUNTER did more than “put his name on the door” and Li’s 2012 visit to New York was unlikely the genesis for a future investment partnership with HUNTER et al.

HUNTER had already met with Bohai Capital’s key stakeholders in several meetings in 2010. He may have met with connected persons during his 2011 trip to China. By 2012, HUNTER, BULGER and ARCHER were already ensconced with the Chinese government and its key financial institutions. Furthermore, the Chinese foreign minister at the time YANG knew BIDEN from his time in

Washington and LIN maintaining clients under the Ministry of Foreign Affairs as Thornton clients. On June 11, Thornton’s LIN met with “senior executives” from Bohai Capital, according to Thornton’s

website.

While Li is not mentioned by name, it is likely he was either present or aware of the meeting.

The future BHR shareholders reportedly signed an agreement in 2013. A photo posted on LIN’s LinkedIn profile shows BIDEN (back row third from left), alongside LIN and BULGER. Media reports

do not specify the date of signature, but FOIA records show that HUNTER visited Shanghai on June 13–14, and then stayed in Beijing until June 15. HUNTER was accompanied by BULGER, LIN, and

ARCHER.

2013 Biden and Hunter visit China and meet BHR CEO LI On December 4, HUNTER accompanies BIDEN on his official trip to China. HUNTER told the New Yorker that he met Li during the December 2013 trip but described it as social encounter. “How do I go to Beijing, halfway around the world, and not see them (Li) for a cup of coffee?” he said. HUNTER arranged a quick meeting in the lobby of the American delegation’s hotel in Beijing between BIDEN and Li, the BHR CEO.

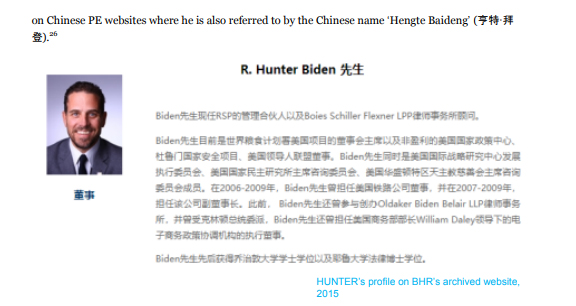

This was followed by a “social meeting” between HUNTER and Li, according to reports by the New Yorker. The trip by HUNTER coincided with an official trip by the Ukranian President Viktor Yanukovych. 22 Many business deals promoting trade and investment between China and Ukraine were signed during this trip. Some deals between Chinese and Ukranian firms have ties to firms HUNTER is known to be involved with such as the Bohai Commodity Exchange, owned by the same local governments that own a part of Bohai Industrial Investment. On 16 December 2013, a week after the BIDEN and HUNTER visit to Beijing, BHR was incorporated in Shanghai, with its registered address in the Shanghai Free Trade Zone, according to State Market Regulatory Administration records. 23 HUNTER’s profile no longer appears on the BHR website.

One archived version lists him as a director on November 16, 2015. 24BIDEN is referred to in the profile as a managing partner of Rosement Seneca Partners and a consultant at Boies Schiller Flexner LPP . According to a statement by BIDEN’s lawyer George Mesires on October 13, 2019, BIDEN was of counsel with Boies Schiller and advising Ukraine-linked Burisma Holdings Limited on its corporate reform initiatives. 25 He is also listed

Lin’s LinkedIn profile and HUNTER’s profile on BHR’s archived website, 2015 SMRA records show HUNTER purchased 10% of BHR on October 23, 2017 (via his investment vehicle Skaneateles LLC) and was a director until April 20, 2020. Previously he was invested via other holding companies. BHR’s current shareholders are Bohai Capital (30%), Shanghai Ample Harvest Financial Services Group Co Ltd (上海丰实金融服务(集团)有限公司) (30%), Angju Investment (10%), Thornton (10%), Ulysses Diversified Inc (10%), Skaneateles LLC (10%). According to Chinese corporate records, the original owner of the US stake in BHR was Rosemont, Seneca Thornton, LLC with a 30% shareholding. This was split just under two years later into what is believed to be 20%/10% holding between Rosemont, Seneca, Bohai LLC and Thornton LLC. This was later changed again splitting Rosemont, Seneca, Bohai into Skanletes and Ulyssees.

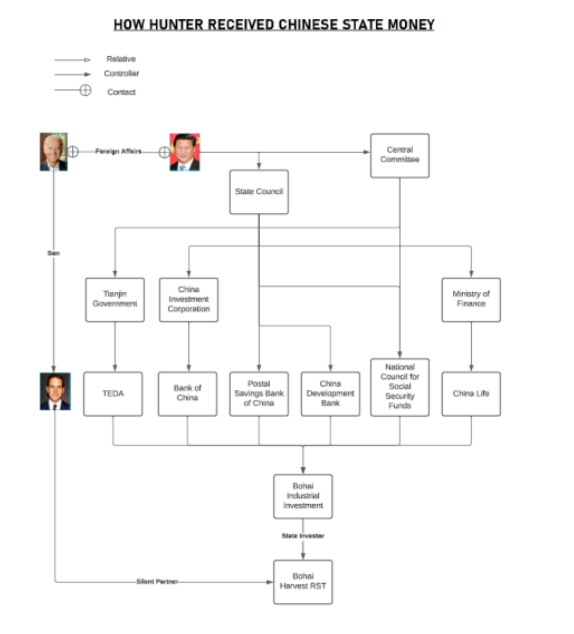

As Rosemont is the HEINZ KERRY vehicle and Seneca is the Biden vehicle, it is believed that the final split allowed HEINZ to exit the partnership divesting to ARCHER. In summary, the Chinese government funded a business that it co-owned along with the son of a sitting US vice president and Secretary of State who was with high probability directly or indirectly invested in the holding company. On May 7 – 8 2014, HUNTER visited China for the fifth time, for undisclosed reasons, according to FOIA records. Bohai Industrial Investment The two Chinese partners Bohai Industrial Investment (Bohai) and Harvest Fund Management (Harvest) are key to understanding the importance of this deal. Bohai is technically a state-owned enterprise (SOE), a specific type of corporate registration, and while Harvest is not an SOE its state linked roots are deep. Understanding these two companies helps us contextualize their importance.

Bohai is owned by a combination of national level SOEs and local governments. In China, there are thousands of local SOEs throughout each city, county, and province but a relatively small number but national SOEs. The financial strength of Bohai comes primarily from its collection of national level SOE financials specifically Bank of China, China Postal Bank, China Development Bank, and National Social Security.

This combination of financial institutions confers upon Bohai both political and financial strength. Together these financial institutions manage nearly $8 trillion USD in financial assets. Relative to China, this gives them financial assets equivalent to approximately 20% of the entire Chinese financial system. Bohai has an enormously deep pool of financial reserves it can easily tap. The financial importance extends two steps further. Much of the financing of BHR projects would be financed primarily by Bohai shareholders via other financial vehicles or products.

China Development Bank and Bank of China specifically appear repeatedly in BHR deals funding their projects throughout China and around the world. Additionally, key personnel from Bohai and BHR come from these institutions speaking to the overlap and relationship between these institutions.

This collection of financial institutions in China also carries clear political implications. These are some of the most politically important SOE’s and financial institutions in China. The Ministry of Finance has a majority direct or indirect stake in almost each case and all are centrally owned.

Each has clear mandates from the central government in a range of areas such as BoC playing the dominant role in foreign exchange clearing and settlement leading them more into international markets, China Postal serving rural customers, and China Development being one of the three banks official policy banks.

Not only is each individual financial institution politically important, a fact not lost on officials and investors, but it also speaks to the specific attempt by official China to work with the princelings of key US public officials. While we do not have specific documentation proving this, based upon well-known Chinese business practice, it seems highly unlikely this influence operation and business deal was not approved at a senior political level given the nature of working with the sons of two highly placed American officials and the historical relationships of Chinese political figures with their fathers.

There is one final channel the political influence appears. Due to the intensely political nature of the financial backing and positioning of Bohai, the deal flow and ultimate projects BHR invests in are effectively Chinese state backed projects. Internationally, BHR invests in projects with officially or nominally Chinese SOE firms. For example, a major international investment involved BHR partnering with AVIC Automotive to purchase Henniges Automotive. Better known as the Aviation Industry Corporation of China (AVIC), AVIC is a vast sprawling military industrial complex company with nearly a half million employees across all its different divisions involved in everything from military aircraft to robotics. AVIC in one form or another has regularly appeared on the US entity list over the years and alleged espionage activities against the US military. AVIC is overseen by SASAC the manager of all state-owned enterprises. Even when the partner or investment is not explicitly a state-owned enterprise it is effectively an SOE. Harvest Fund Management is technically a private company but receives significant backing from major state linked entities which have received public bailouts. One of the major shareholders in Harvest is a financial firm named China Credit Trust (CCT). CCT is a financial non-depository financial firm owned by a group of composed of provincial and national level coal and mining companies. The national SOE’s are major firms including the China National Coal Group, China People’s Insurance, and China Minmetals all directly under the powerful SASAC. Like the backing for Bohai, the backing for Harvest is very similarly state owned and linked. The multilayered links to the state extends to investment. Despite the publicly stated reason for the investment fund to focus on international ventures, the large majority of investment flows to domestic 27 It is worth noting, technically Bank of China is considered to have made two separate investments coming from different business units into Bohai which when combined give BoC 53% of total equity.

Not only is total fund investment primarily domestic but it appears to flow primarily to public private or policy linked investment. Public-private investment in China consists of infrastructure, public works, and policy driven investment linked to government interests. This may consist of everything from toll roads to convention centers and investment funds, similar to Bohai, that are designed to stimulate activity. The central government also publishes regular lists of strategic industries that are to receive preferential access to capital. Public private investment in China has increased rapidly as local governments face restrictions on official public debt limits. To skirt central government rules that limit debt growth but still meet investment targets, local governments create off public balance sheet vehicles consisting of state linked companies with loans from banks or trust firms that provide investment capital. The flow of capital to public-private or strategic projects is notable in this case as it provides further evidence of the state link between BHR and its purpose. The supposed purpose of the BHR partnership documents was for Chinese capital to invest abroad but records show most of invested domestically in state backed projects. Consequently, there appears no viable business reason for a foreign investor due to the primarily state backed nature of the investment and it effectively guarantees the investment.

The close links between the fund and the Chinese state at all levels raise valid and worrying concerns. The original partnership stems from an individual working closely with official Chinese state enterprises and government agencies, brought in major SOEs, invested in state policy projects both internationally and domestically effectively guaranteeing a return for investors.

At every level the BHR partnership is linked to the Chinese state. Valuing the Partnership A key question surrounding the BHR partnership concerns the value of the partnership and the underlying financing provided to the partnership by Chinese state linked financial firms.

It should be noted at the outset that given the lack of documentation such as fee schedule and partnership agreement that will have significant impact on valuation and financial flows, we lack important details that would help us provide greater specificity and certainty about financial aspects of the BHR partnership.

Where we lack detail that cannot be directly obtained about BHR, we will use industry standard or provide various scenarios based upon potential missing details. The first major question about BHR financials concerns the size of the firm’s business.

Most news reports have placed the value of assets under management (AUM) at BHR at $1-1.5 billion USD. This number is likely to be significantly lower than reality. If we take just two international transactions, Tenke Fungurume mine in the DRC and the Henniges Automotive purchase in total sum to approximately $1.6 billion USD leaving aside all other less public projects and various financing details which remain unknown but pertinent.

Put another way, if we consider only two simultaneous projects, the total AUM would exceed the previously public estimates of BHR. There is a more direct and likely more reliable estimate of $6.5 billion USD for the current AUM of BHR. Thornton co-founder LIN listing himself as a BHR co-cofounder declares total assets under management (AUM) as $6.5 billion USD on his personal LinkedIn page. It is difficult to verify this statement because many BHR projects do not provide public financials or announcements.

However, given the less conspicuous nature of the statement and his ability to make such a statement, it should be taken as credible given its first-person testimony as to the state of the business. Importantly, this puts the true nature of AUM as more than four times higher than previous estimates. This has a major impact on the valuation both in year to year cash flow terms and in terms of capital appreciation gains that would accrue to partners.

Private equity firms typically make money through two different channels in what is known in the industry as a 2/20 fee schedule. Private equity firms like BHR first receive annual management fee of 2% of committed or managed capital depending on the partnership agreement.

If we assume that BHR receives annual revenue of 2% of $6.5 billion then this would amount to $130 million USD annually in ongoing management fees. According to BHR, they report the number the number of employees between 11-50 while news reports report the number at 20. Taking the high number of employees at fifty, this would place the annual fee revenue, excluding capital gains and similar revenue, per employee at approximately $2.6 million per employee.

Taking the news report number of 20 employees, that would place revenue per worker at $6.5 million. However, for multiple reasons most private equity firms make their big payouts from taking a percentage of capital appreciation gains. The standard fee is 20% of gains when the rate of return exceeds a specific hurdle rate. Let us take very simple example to illustrate the potential payout for BHR.

Let us assume that BHR wishes to liquidate current assets and finds buyers willing to pay $8 billion USD for its assets currently listed at $6.5 billion. Assuming this exceeds the required hurdle rate, BHR would realize a payout of 20% of $1.5 billion or $300 million. Private equity firms, and similar financial firms like hedge funds, are extremely difficult to value for asset purchase purposes due to the inherent volatility and human capital focus of key personnel.

However, it would be clear that even just on a management fee basis, the firm generates significant yearly revenue and would likely realize significant capital gains for partner distribution. There are additional factors that make the BHR business difficult to value both for any asset sale and business sale as a going concern. There is effectively no open market for BHR assets or business. Given that the majority of their assets are now public projects or co-investments with major SOE’s there is effectively no open market for BHR assets. BHR cannot liquidate its assets without Beijing or local government approval and the price is determined by the primary counter party rather than market valuation.

The same holds for any valuation of BHR as a going concern. Given the SOE direct ownership and project financing, any purchaser would be dependent on the good will received by the politically connected owners. Any sale of BHR assets or the business is effectively a Chinese state decision.

This returns the entire partnership to the fundamental problem: two sons of the Vice President of the United States and the Secretary of State willingly entered into a financial partnership with a government their fathers were supposed to deal with in an impartial manner.

Evidence indicates that the Secretary of State was directly or indirectly financially invested in his son’s firms and benefitted from asset purchases made by firms directly linked to his son.

HUNTER invested in a firm that by his own words has had almost nothing to do with, managed by state government with departments dedicated to elite capture, focusing on state enterprise deals in a foreign country, but has grown to manage $6.5 billion in assets and likely realize yearly revenue of $100-150 million. The ultimate sale price for his stake or the partnership would be whatever the Chinese Communist Party decides his partnership stake is worth. 2016 BHR DEALS The 30% stake in BHR held by Rosemont, Seneca, Thornton was split into two separate holdings.

The new holding of the US partners are now split between Rosemont, Seneca, Bohai LLC and Thornton Group LLC. On September 15, BHR and AVIC Auto acquired US automotive supplier Henniges Automotive with a 49% share and 51% share respectively, according to a press release. 28AVIC Auto, which is described in the press release as BHR’s joint venture partner, is a subsidiary of AVIC.

Henniges described the deal as “one of the largest acquisitions by a Chinese company of a U.S.-based automotive manufacturing company in history”. 2016 On September 8, China Molybdenum entered into an agreement with Freeport McMoran to purchase 56% of a holding company with ownership of an operational mine in the Democratic Republic of the Congo with BHR purchasing an additional 24%. China Moly and BHR act in concert with China Moly acting as the managing partner bringing their stake in the mine to 80%. China Moly agreed to purchase the Tengke Fungurume cobalt and copper mine from Freeport McMoran in 2016 with BHR acting a co-investor. China Moly purchased 56% with BHR purchasing an additional 24%. Despite the appearances of an international free market arm’s length transaction, this is effectively a state backed investment.

The major shareholder in China Moly is a beneficial owner for the State-Owned Assets Supervision and Administration Commission of the State Council of China (SASAC).

This follows the pattern the BHR is created with central SOE involvement and partners with state owned or linked entities. There are a few unique facets of this specific investment. China Moly effectively guaranteed the investment for BHR engaging in uniquely non-market behavior. The deal between China Moly and BHR was a complicated transaction that gave China Moly a call option and BHR a put option.

This effectively guaranteed a specified rate of return to BHR. Adding to this, China Moly guaranteed a loan up to $700 million received by BHR from China Construction Bank.

The agreement goes even further to compensate BHR investors if BHR cannot raise the required capital for investment, even with China Moly assets guaranteeing the transaction, “compensate(ing) BHR for losses it suffers as a result…”. Given the China Moly guaranteed rate of return to BHR and the guarantee of capital for BHR to fund its share of the investment, this is cannot be considered a market-based transaction. BHR provided no value to the transaction and the special purpose vehicle in this transaction was subsequently considered a subsidiary of China Moly in accounting records. BHR eventually secured investors for their share of capital.

The specific investors brought in by BHR however are also notable. 31 Two of the specific investors were linked to Chinese state-owned funds investing in Africa. Another investor, Design Time Limited, remains an unknown entity beyond its name due to incorporating in a jurisdiction with a company known for protecting the anonymity of high powered Chinese individuals and institutions. It is possible to say however, based upon their other holdings that Design Time is a very powerful entity in their own right whoever owns them.

Design Time is listed as an equal owner to China Construction Bank in companies owned by the centrally owned Central Huijin Investment. 32 Central Huijin is the domestically focused subsidiary of the China Investment Corporation owned and overseen by the Ministry of Finance. Whoever owns Design Time Limited is without question a major politically and financially important institution or individual. The final company, named as CNBC (Hong Kong) Investment Limited does not actually appear anywhere in Hong Kong corporate records. China Moly purchased the outstanding 24% from BHR less than two years after entering into this partnership. The two-year timeline is notable because in the bank loan agreement BHR reached with China Construction Bank, the China Moly guarantee only extended two years. Since this time, China Moly has declared the Tengke Fungurume mine unprofitable at current prices that began sliding when they entered into the 2019 purchase agreement and have continued since. Based upon existing evidence, BHR involvement seems less about value creation and generating investment returns for preferred individuals.

2015 Hunter’s Third China Deal – Sino-Ocean 2015 In 2015, Rosemont Realty was acquired by Gemini Investments, which is wholly-owned by Hong Kong listed PRC real estate developer, Sino-Ocean. 33 Rosemont Realty were promised USD 3 billion as part of the deal for its US commercial property portfolio. 34 Notably, KERRY through family trusts, was likely either directly or indirectly invested in Rosemont Realty. In other words, the Chinese government purchased a business from a relative of the Secretary of State in which they were likely invested, while also being the major financier for the Vice-President’s son (via BHR).

A representative of Gemini Rosemont issued this statement in 2019: “Hunter Biden had a brief relationship with Rosemont Realty and was on its advisory board from 2010 to 2014. Gemini Rosemont was formed after that relationship with Hunter Biden ended and Gemini Rosemont has never had a relationship with Hunter Biden. We do not know about his af iliations with other companies, other than what we read in the news.” 35Clearly Hunter’s top-level Chinese connections, in particular with China Life the largest owned of Sino-Ocean and its subsidiary Gemini, would have helped seal the deal, even though he quit before it was announced.

2012 Archer’s China Deal – Sichuan Chemical on October 29, Thornton’s LIN visited local government officials in Xinjiang meeting with executives from Sichuan Chemical for the second time. 36 One week prior on October 22, a press release announced that Sichuan Chemical had signed a USD 2- billion 10-year agreement to purchase 500,000 metric tons of potash annually from Prospect Global Resources Inc (NASDAQ: PGRX), equivalent to 25% of the projected output. 37 ARCHER was a Prospect Global director and the lead negotiator in the deal. He commented that “Today’s agreement is the product of six months of negotiation and due diligence carried out in China and the United States. That process has resulted in a high level of trust and respect on the part of both parties. As we look forward to a long relationship with Sichuan Chemical, we are proud of the role that Prospect Global can play in helping to bring food security to China while meaningfully impacting the US/China trade balance over the next decade.” In its SEC filings, Prospect Global noted that the deal was subject final approval by the Sichuan Provincial Government and affiliates, confirming that this was a deal between ARCHER’s company and the Sichuan government. 38 ARCHER was only on the board of directors from March 2012 to November 2012, according to SEC filings, but received compensation worth approximately USD 3 million. 39 The deal with Sichuan Chemical appears to be Prospect Global’s only announced deal. The company was delisted from NASDAQ on July 10, 2014 and its website is no longer live. 40 This implies that ARCHER and Prospect Global began negotiations with Sichuan Chemical a few months after BIDEN’s visit to Sichuan, while at the same time, LIN was meeting with Sichuan Chemical executives. It is unlikely that all parties, including BIDEN, were unaware of the others actions, 33 3377.

2019 Biden denies knowledge of Hunter’s China Deals 2019 On May 2, BIDEN remarked, “They can’t figure out how they’re going to deal with the corruption that exists within the system. I mean, you know, they’re not bad folks, folks. But guess what, they’re not, they’re not competition for us.” On May 3, it was reported that BHR invested in Face++, a Chinese surveillance company which develops facial-recognition software for law enforcement in China, including targeting ethnic minority Muslims Xinjiang.